Community, Diversity, Sustainability and other Overused Words

Community, Diversity, Sustainability and other Overused Words

Inherited assets from your loved one, whether in the form of cash, stocks or real estate, can be subject to inheritance taxes, depending on your relationship and inheritance value

Inherited assets from your loved one, whether in the form of cash, stocks or real estate, can be subject to inheritance taxes, depending on your relationship and inheritance value. While most states don’t charge such taxes, those that do have their own rules for the rates and exemptions.

Additionally, reducing inheritance taxes is possible, provided the owner of the assets is still alive to make the arrangements. As a taxpayer, you may also take advantage of certain state discounts. In this article, Inheritance Funding discusses when you need to pay inheritance taxes and how you can avoid or reduce them.

The maximum tax-free amount you can inherit depends on state rules — there is currently no federal inheritance tax. Spouses, children and other persons considered Class A or Class 1 beneficiaries or heirs are usually exempt from such taxes. Beneficiaries are those named in a person’s will inheriting the assets, while heirs are persons receiving such assets if there is no will.

The more distant your relationship is, the higher your potential tax rates. Inheritance taxes may also apply if the inherited property is located in a state that charges them, even if you or your loved one does not reside in this state.

The estate refers to the totality of your loved one’s assets. It can be subject to estate taxes, depending on its total value, where payments will come from the assets within the estate. In contrast, you, as a beneficiary, will pay for the inheritance taxes. These payments are usually managed by an executor of a will — the person responsible for distributing the assets — or a court-appointed personal representative.

The federal estate tax exemption for 2025 is $13.99 million per person. Because this limit is such a huge amount, only a small percentage of estates are often subject to estate taxes. The amount that exceeds the limit can be charged at up to 40%.

Twelve states and the District of Columbia charge estate taxes, while five states impose inheritance taxes. States with estate taxes include:

States with inheritance taxes include:

Iowa repealed its state inheritance tax for deaths in 2025. For deaths that occurred in 2024, an inheritance tax is due if the estate’s value is $25,000 or more. Here’s what the other states require.

Kentucky categorizes three classes of beneficiaries.

Class A:

Class B:

Class C:

Class A beneficiaries are exempt from inheritance tax, while those in Class B get a tax rate of 4% to 16% and a $1,000 exemption. Class C beneficiaries have a tax rate of 6% to 16% with a $500 exemption. If you pay the inheritance tax within nine months of your loved one’s passing, you can get a 5% discount. If the amount due is more than $5,000, filed timely, you can pay the amount in 10 equal yearly installments.

All properties in Kentucky are subject to inheritance tax, even if your loved one is not a Kentucky resident.

In Maryland, if the property you will inherit has a value of up to $1,000, you may not be subject to inheritance tax. You are also tax-exempt if you are your loved one’s:

Collateral heirs, which include nieces, nephews, aunts, uncles and cousins, must pay a 10% inheritance tax. The same rate applies to other individuals not related by blood.

Maryland charges inheritance taxes for all properties your loved one owned, controlled and benefited from upon their passing. This includes properties they co-owned and those included in the will. Exemptions include:

Nebraska also categorizes beneficiaries into three classes:

Class 1:

Class 2:

Class 3:

Lineal descendants are direct descendants of a person, such as children and grandchildren. States typically consider adopted children as lineal descendants, while many states don’t consider biological children the same if they have been adopted by other adults.

Class 1 beneficiaries get a 1% tax rate on amounts they receive over $100,000. Class 2 beneficiaries get 11% for amounts over $40,000. Those in Class 3 get 15% on amounts over $25,000. All beneficiaries under 22 years old are fully exempted.

The inheritance tax is based on the fair market value of the assets. The taxes apply to all gifts made at death, directly or through a trust, and certain rights, like annuities and life estates.

New Jersey has a graduated inheritance tax for real and personal properties with an aggregate value of $500 or more. Life insurance proceeds are exempt from this tax. Like other states, New Jersey categorizes beneficiaries into three classes, excluding Class B, which was eliminated on July 1, 1963.

Class A:

Class C:

Class D:

Class A beneficiaries are exempt from inheritance tax, while Class C beneficiaries have the following rates.

Class D beneficiaries get the following rates.

Properties in New Jersey, whether your loved one is a resident or not, can be taxed.

Pennsylvania doesn’t charge inheritance taxes on the spouse and parents of children 21 years old or younger. However, the following rates apply to other beneficiaries:

Inheritance tax exemptions include:

Paying the required amount within three months of your loved one’s passing can get you a 5% discount. Payments become delinquent after nine months.

Each state with inheritance taxes has its own exemption rules. Usually, the surviving spouse, children and other Class A or Class 1 beneficiaries are exempt from the tax. Some entities, such as charitable and religious institutions, may also be exempt, depending on the state.

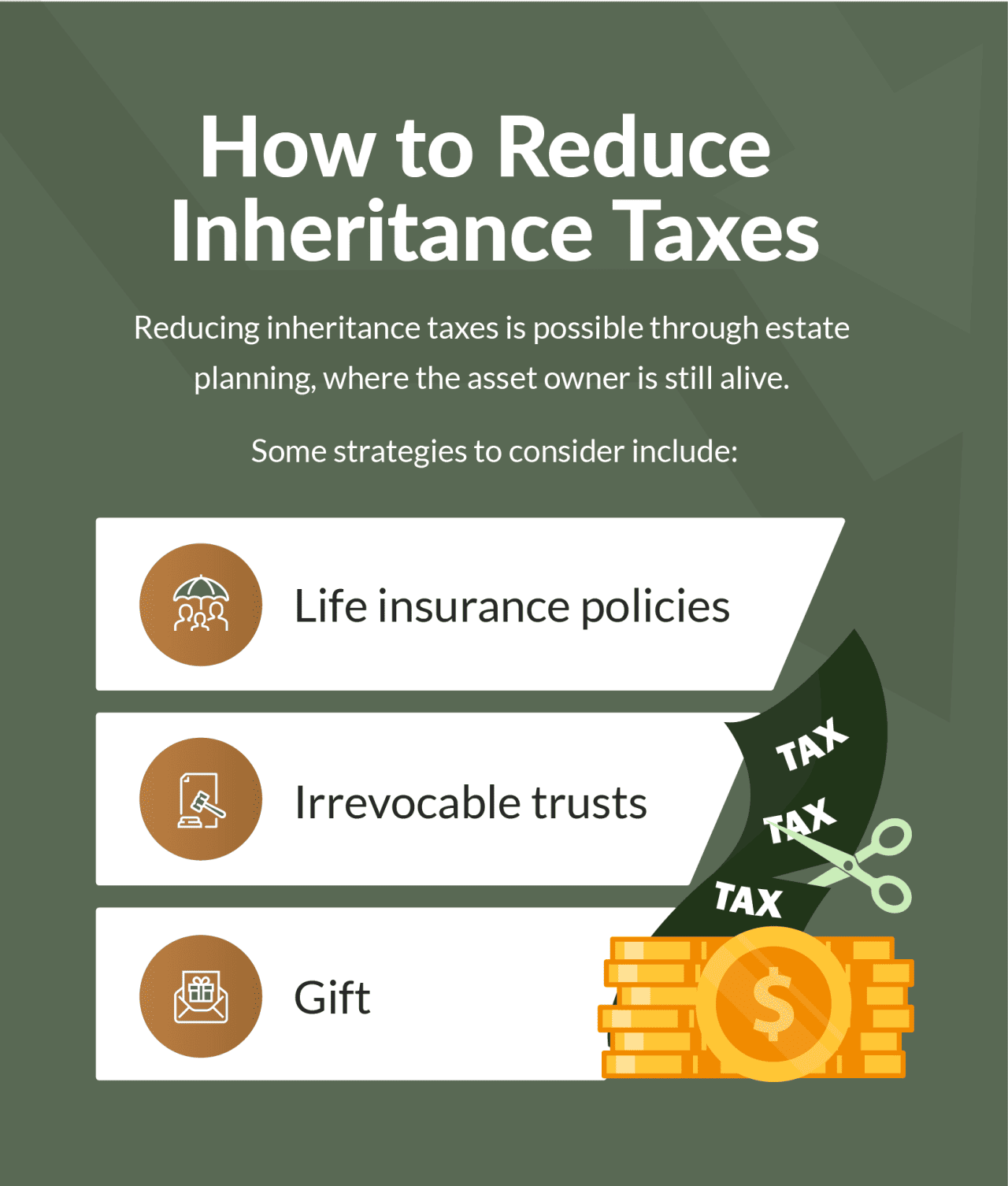

Reducing inheritance taxes is possible through estate planning, where the asset owner is still alive. The goal is to reduce the number of assets your loved one passes on upon their death. Some strategies to consider include the following.

Some states set periods during which assets gifted a few years before the owner’s passing can still be subject to an inheritance tax, as they may have been transferred in contemplation of death. For instance, in Nebraska, gifts made within three years prior to the owner’s death can be subject to an inheritance tax. When planning to distribute assets to reduce taxes, consider the relevant state’s statutory lookback.

Payment instructions vary per state, including the filing authorities responsible and deadlines. Here’s how the five states differ.

To further understand inheritance taxes and how you can work around them, consider these questions and answers.

Do I need to report inheritance money to the IRS?

An inheritance is not considered taxable income, so you don’t need to report what you receive to the IRS. The executor or personal representative is responsible for filing the inheritance tax return. However, you may need to report earnings you receive from the inheritance.

What is the loophole of the inheritance tax?

The loophole for inheritance taxes refers to the step-up basis rule. Once you inherit the assets, their value is stepped up to the fair market value at the time of your loved one’s passing. This can reduce the inheritance tax you owe and the capital gains tax if you sell the assets later on, provided the asset has appreciated in value from its initial purchase.

States use the asset’s fair market value in determining the inheritance tax. Because the adjusted value reflects a smaller profit, you’ll also owe less in capital gains tax.

Can I gift money to avoid inheritance tax?

Yes, you can gift money or other assets to reduce or avoid inheritance tax. You only need to remember your state’s statutory lookback, as gifts given a few years before the owner’s passing can still be charged.

Most states don’t charge inheritance taxes. However, for those who do, the amount of money you can inherit before owing taxes depends on each state. States with inheritance taxes include:

Beneficiaries closely related to the person who passed, usually called Class A or Class 1 beneficiaries, are often exempt from the taxes. Distant relatives and persons not related by blood may be charged higher rates. Reducing or avoiding inheritance taxes is possible, but only if the original owner is still living to distribute the assets before their death. Otherwise, consider paying the taxes early to potentially qualify for a discount. Some states may also permit installment payments for larger tax amounts.

This story was produced by Inheritance Funding and reviewed and distributed by Stacker.

Reader Comments(0)